import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_squared_error

import statsmodels.api as sm

import statsmodels.formula.api as smf

loans = pd.read_csv('data/loans_full_schema.csv')AE 11: Modelling loan interest rates

Application exercise

In this application exercise we will be studying loan interest rates. The dataset is one you’ve come across before in your reading – the dataset about loans from the peer-to-peer lender, Lending Club, from the openintro R package. We will use pandas and scikit-learn for data exploration and modeling, respectively.

Before we use the dataset, we’ll make a few transformations to it.

- Your turn: Review the code below and write a summary of the data transformation pipeline.

Answer:

The code performs several data cleaning and feature engineering steps: - Creates credit_util as a ratio of credit used to total credit limit. - Transforms public_record_bankrupt into a binary categorical variable bankruptcy. - Converts verified_income and homeownership to categorical variables, with homeownership set as an ordered category. - Renames inquiries_last_12m to credit_checks. - Filters the dataset to retain only the relevant variables for analysis.

loans['credit_util'] = loans['total_credit_utilized'] / loans['total_credit_limit']

loans['bankruptcy'] = loans['public_record_bankrupt'].apply(lambda x: 0 if x == 0 else 1).astype('category')

loans['verified_income'] = loans['verified_income'].astype('category')

loans['homeownership'] = loans['homeownership'].str.title().astype('category')

loans['homeownership'] = pd.Categorical(loans['homeownership'], categories=["Rent", "Mortgage", "Own"], ordered=True)

loans = loans.rename(columns={'inquiries_last_12m': 'credit_checks'})

loans = loans[['interest_rate', 'loan_amount', 'verified_income', 'debt_to_income', 'credit_util', 'bankruptcy', 'term', 'credit_checks', 'issue_month', 'homeownership']]Here is a glimpse at the data:

print(loans.info())

print(loans.describe())<class 'pandas.core.frame.DataFrame'>

RangeIndex: 10000 entries, 0 to 9999

Data columns (total 10 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 interest_rate 10000 non-null float64

1 loan_amount 10000 non-null int64

2 verified_income 10000 non-null category

3 debt_to_income 9976 non-null float64

4 credit_util 9998 non-null float64

5 bankruptcy 10000 non-null category

6 term 10000 non-null int64

7 credit_checks 10000 non-null int64

8 issue_month 10000 non-null object

9 homeownership 10000 non-null category

dtypes: category(3), float64(3), int64(3), object(1)

memory usage: 576.7+ KB

None

interest_rate loan_amount debt_to_income credit_util term \

count 10000.000000 10000.000000 9976.000000 9998.000000 10000.000000

mean 12.427524 16361.922500 19.308192 0.403158 43.272000

std 5.001105 10301.956759 15.004851 0.269313 11.029877

min 5.310000 1000.000000 0.000000 0.000000 36.000000

25% 9.430000 8000.000000 11.057500 0.169029 36.000000

50% 11.980000 14500.000000 17.570000 0.360192 36.000000

75% 15.050000 24000.000000 25.002500 0.607317 60.000000

max 30.940000 40000.000000 469.090000 1.835280 60.000000

credit_checks

count 10000.00000

mean 1.95820

std 2.38013

min 0.00000

25% 0.00000

50% 1.00000

75% 3.00000

max 29.00000 Get to know the data

- Your turn: What is a typical interest rate in this dataset? What are some attributes of a typical loan and a typical borrower. Give yourself no more than 5 minutes for this exploration and share 1-2 findings.

# Explore loan-related variables

loans[['interest_rate', 'loan_amount', 'debt_to_income', 'credit_util']].describe()| interest_rate | loan_amount | debt_to_income | credit_util | |

|---|---|---|---|---|

| count | 10000.000000 | 10000.000000 | 9976.000000 | 9998.000000 |

| mean | 12.427524 | 16361.922500 | 19.308192 | 0.403158 |

| std | 5.001105 | 10301.956759 | 15.004851 | 0.269313 |

| min | 5.310000 | 1000.000000 | 0.000000 | 0.000000 |

| 25% | 9.430000 | 8000.000000 | 11.057500 | 0.169029 |

| 50% | 11.980000 | 14500.000000 | 17.570000 | 0.360192 |

| 75% | 15.050000 | 24000.000000 | 25.002500 | 0.607317 |

| max | 30.940000 | 40000.000000 | 469.090000 | 1.835280 |

# Explore borrower-related variables

loans['verified_income'].value_counts(normalize=True)

loans['homeownership'].value_counts(normalize=True)

loans['bankruptcy'].value_counts(normalize=True)bankruptcy

0 0.8785

1 0.1215

Name: proportion, dtype: float64Answer - The typical interest rate (mean) is around 12.43%, with most loans ranging between 9.43% and 15.05%.

Most borrowers have Verified/Source Verified income, no bankruptcy, and either rent or have a mortgage.

The average debt-to-income ratio is around 19.3%, and credit utilization is around 40.3%.

Interest rate vs. credit utilization ratio

Python does not encode categories or handle missing values for you. Linear regression models are incapable of handling either, so we will need to use one-hot encoding to encode categories and drop missing values.

Hint: Python also does not convert the one-hot encoded values to numerics… so we must do this as well.

X = loans[['credit_util', 'homeownership']]

X = pd.get_dummies(X, drop_first=True)

X = X.dropna()

X = X.replace([np.inf, -np.inf], np.nan).dropna()

X = X.astype(float)

y = loans.loc[X.index, 'interest_rate']

y = y.dropna()The regression model for interest rate vs. credit utilization is as follows.

X = sm.add_constant(X)

model = sm.OLS(y, X).fit()

print(model.summary2()) Results: Ordinary least squares

=====================================================================

Model: OLS Adj. R-squared: 0.068

Dependent Variable: interest_rate AIC: 59859.3779

Date: 2025-05-05 17:48 BIC: 59888.2185

No. Observations: 9998 Log-Likelihood: -29926.

Df Model: 3 F-statistic: 243.7

Df Residuals: 9994 Prob (F-statistic): 1.25e-152

R-squared: 0.068 Scale: 23.309

---------------------------------------------------------------------

Coef. Std.Err. t P>|t| [0.025 0.975]

---------------------------------------------------------------------

const 9.9250 0.1401 70.8498 0.0000 9.6504 10.1996

credit_util 5.3356 0.2074 25.7266 0.0000 4.9291 5.7421

homeownership_Mortgage 0.6956 0.1208 5.7590 0.0000 0.4588 0.9323

homeownership_Own 0.1283 0.1552 0.8266 0.4085 -0.1760 0.4326

---------------------------------------------------------------------

Omnibus: 1150.070 Durbin-Watson: 1.981

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1616.376

Skew: 0.900 Prob(JB): 0.000

Kurtosis: 3.800 Condition No.: 6

=====================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors

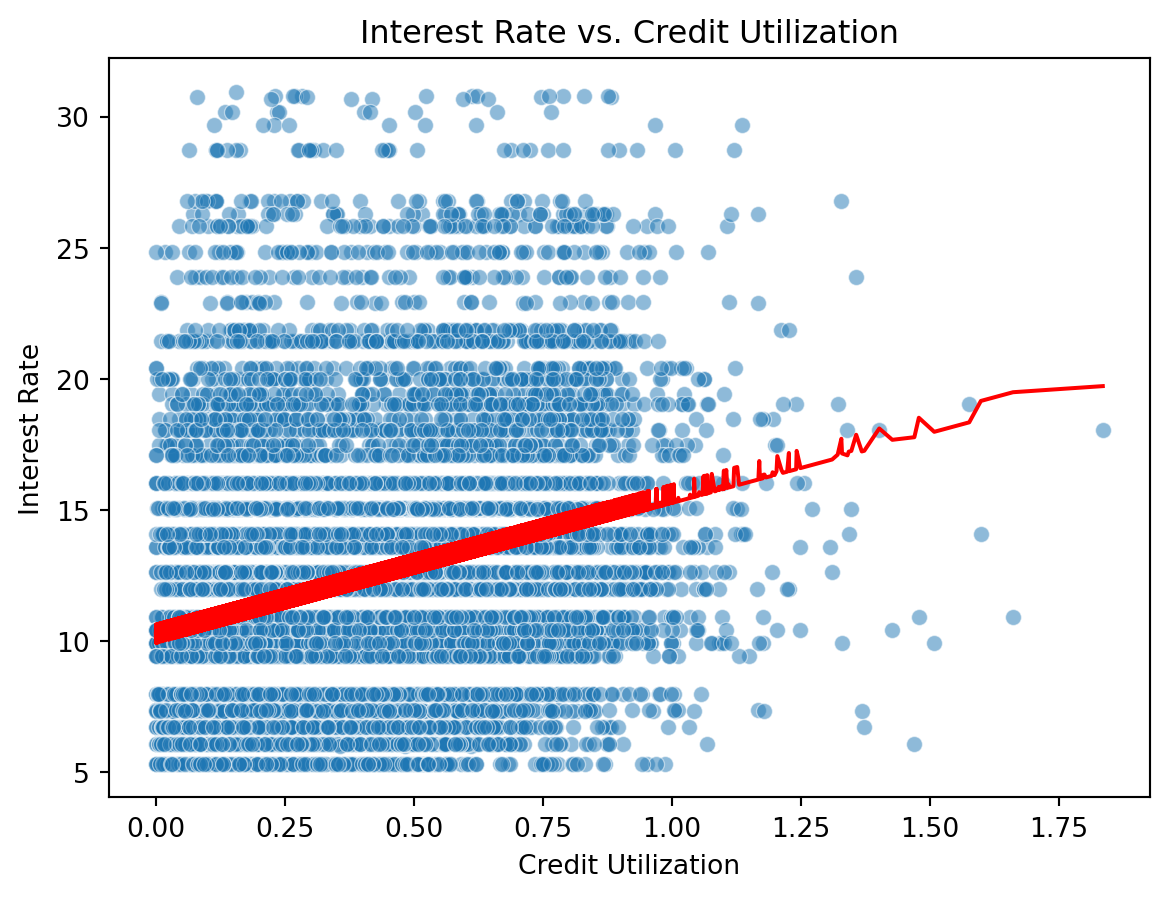

is correctly specified.And here is the model visualized:

sns.scatterplot(x='credit_util', y='interest_rate', data=loans, alpha=0.5)

sns.lineplot(x=loans['credit_util'], y=model.predict(X), color='red')

plt.xlabel('Credit Utilization')

plt.ylabel('Interest Rate')

plt.title('Interest Rate vs. Credit Utilization')

plt.show()

- Your turn: Interpret the intercept and the slope.

Answer Intercept: Renters with 0 credit utilization are predicted to have an interest rate of 9.93%.

Slope: For every 1.0 increase in credit utilization (which corresponds to a 100 percentage point increase — an unrealistic but technically accurate unit), the interest rate increases by 5.34 percentage points..

Interest rate vs. homeownership

Next we predict interest rates from homeownership, which is a categorical predictor with three levels:

homeownership_levels = loans['homeownership'].cat.categories

print(homeownership_levels)Index(['Rent', 'Mortgage', 'Own'], dtype='object')- Fit the linear regression model to predict interest rate from homeownership and display a summary of the model. Write the estimated model output below.

# Fit linear regression model

model_homeownership = smf.ols('interest_rate ~ C(homeownership)', data=loans).fit()

# Display summary

model_homeownership.summary()| Dep. Variable: | interest_rate | R-squared: | 0.006 |

| Model: | OLS | Adj. R-squared: | 0.006 |

| Method: | Least Squares | F-statistic: | 32.65 |

| Date: | Mon, 05 May 2025 | Prob (F-statistic): | 7.35e-15 |

| Time: | 17:48:39 | Log-Likelihood: | -30253. |

| No. Observations: | 10000 | AIC: | 6.051e+04 |

| Df Residuals: | 9997 | BIC: | 6.053e+04 |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

| Intercept | 12.9250 | 0.080 | 161.033 | 0.000 | 12.768 | 13.082 |

| C(homeownership)[T.Mortgage] | -0.8661 | 0.108 | -8.030 | 0.000 | -1.078 | -0.655 |

| C(homeownership)[T.Own] | -0.6110 | 0.158 | -3.879 | 0.000 | -0.920 | -0.302 |

| Omnibus: | 1045.136 | Durbin-Watson: | 1.990 |

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 1408.154 |

| Skew: | 0.866 | Prob(JB): | 1.67e-306 |

| Kurtosis: | 3.615 | Cond. No. | 3.99 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

- Your turn: Interpret each coefficient in context of the problem.

Answer * All coefficients are statistically significant (p < 0.001), suggesting that homeownership status meaningfully affects predicted interest rates.

Borrowers who don’t rent (i.e., have a mortgage or own) tend to get slightly lower interest rates, possibly due to being perceived as more financially stable or less risky.

The overall R-squared is low (0.006), so homeownership alone doesn’t explain much of the variance in interest rates — but it still has a measurable effect.

Interest rate vs. credit utilization and homeownership

Main effects model

- Fit a model to predict interest rate from credit utilization and homeownership, without an interaction effect between the two predictors. Display the summary output and write out the estimated regression equation.

# Fit linear regression model: interest_rate ~ credit_util + homeownership (no interaction)

model_main_effects = smf.ols('interest_rate ~ credit_util + C(homeownership)', data=loans).fit()

# Display summary

model_main_effects.summary()| Dep. Variable: | interest_rate | R-squared: | 0.068 |

| Model: | OLS | Adj. R-squared: | 0.068 |

| Method: | Least Squares | F-statistic: | 243.7 |

| Date: | Mon, 05 May 2025 | Prob (F-statistic): | 1.25e-152 |

| Time: | 17:48:39 | Log-Likelihood: | -29926. |

| No. Observations: | 9998 | AIC: | 5.986e+04 |

| Df Residuals: | 9994 | BIC: | 5.989e+04 |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

| Intercept | 9.9250 | 0.140 | 70.850 | 0.000 | 9.650 | 10.200 |

| C(homeownership)[T.Mortgage] | 0.6956 | 0.121 | 5.759 | 0.000 | 0.459 | 0.932 |

| C(homeownership)[T.Own] | 0.1283 | 0.155 | 0.827 | 0.408 | -0.176 | 0.433 |

| credit_util | 5.3356 | 0.207 | 25.727 | 0.000 | 4.929 | 5.742 |

| Omnibus: | 1150.070 | Durbin-Watson: | 1.981 |

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 1616.376 |

| Skew: | 0.900 | Prob(JB): | 0.00 |

| Kurtosis: | 3.800 | Cond. No. | 6.48 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

- Write the estimated regression equation for loan applications from each of the homeownership groups separately.

- Rent:

- Mortgage:

- Own:

- Rent:

Answer:

The slope for

credit_utilis the same across all groups: 5.336.

This means that as credit utilization increases, interest rates increase at the same rate, regardless of homeownership status.The difference lies in the intercepts:

- Renters start at 9.93%

- Mortgage holders start higher, at 10.62%

- Homeowners who own outright start at 10.05%, but this difference is not statistically significant (p = 0.41)

Conclusion:

While credit utilization has a consistent impact on interest rate across all groups, the baseline rate varies slightly by homeownership — with mortgage holders paying the most on average. However, the effect of owning outright is minimal and not significant in this model.

Interaction effects model

- Fit a model to predict interest rate from credit utilization and homeownership, with an interaction effect between the two predictors. Display the summary output and write out the estimated regression equation.

# Fit linear regression model with interaction

model_interaction = smf.ols('interest_rate ~ credit_util * C(homeownership)', data=loans).fit()

# Display summary

model_interaction.summary()| Dep. Variable: | interest_rate | R-squared: | 0.069 |

| Model: | OLS | Adj. R-squared: | 0.069 |

| Method: | Least Squares | F-statistic: | 149.0 |

| Date: | Mon, 05 May 2025 | Prob (F-statistic): | 4.79e-153 |

| Time: | 17:48:39 | Log-Likelihood: | -29919. |

| No. Observations: | 9998 | AIC: | 5.985e+04 |

| Df Residuals: | 9992 | BIC: | 5.989e+04 |

| Df Model: | 5 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

| Intercept | 9.4369 | 0.199 | 47.526 | 0.000 | 9.048 | 9.826 |

| C(homeownership)[T.Mortgage] | 1.3903 | 0.228 | 6.109 | 0.000 | 0.944 | 1.836 |

| C(homeownership)[T.Own] | 0.6972 | 0.316 | 2.204 | 0.028 | 0.077 | 1.317 |

| credit_util | 6.2043 | 0.325 | 19.077 | 0.000 | 5.567 | 6.842 |

| credit_util:C(homeownership)[T.Mortgage] | -1.6354 | 0.457 | -3.577 | 0.000 | -2.532 | -0.739 |

| credit_util:C(homeownership)[T.Own] | -1.0594 | 0.590 | -1.797 | 0.072 | -2.215 | 0.096 |

| Omnibus: | 1157.460 | Durbin-Watson: | 1.984 |

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 1630.777 |

| Skew: | 0.903 | Prob(JB): | 0.00 |

| Kurtosis: | 3.808 | Cond. No. | 19.2 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

- Write the estimated regression equation for loan applications from each of the homeownership groups separately.

- Rent:

- Mortgage:

- Own:

- Rent:

- Question: How does the model predict the interest rate to vary as credit utilization varies for loan applicants with different homeownership status. Are the rates the same or different?

Answer:

No, the rates are not the same — the effect of credit utilization on interest rate varies depending on homeownership status, due to the interaction terms:

- Renters: Each 1-unit increase in credit utilization increases the interest rate by 6.20 percentage points.

- Mortgage holders: The slope is reduced to 4.57, meaning their interest rates increase more slowly with higher credit utilization.

- Owners: The slope is 5.15, slightly lower than renters but higher than mortgage holders.

Conclusion:

Renters are penalized most steeply for higher credit utilization, while those with a mortgage experience a more modest rate increase. This suggests that homeownership moderates the impact of credit utilization, likely because lenders view homeowners as lower-risk borrowers.

Choosing a model

Rule of thumb: Occam’s Razor - Don’t overcomplicate the situation! We prefer the simplest best model.

# Compare the main effects model and the interaction model

print("Main effects model AIC:", model_main_effects.aic)

print("Interaction effects model AIC:", model_interaction.aic)

print("Main effects model Adj. R²:", model_main_effects.rsquared_adj)

print("Interaction model Adj. R²:", model_interaction.rsquared_adj)Main effects model AIC: 59859.377892328295

Interaction effects model AIC: 59850.400228039085

Main effects model Adj. R²: 0.0678893487525869

Interaction model Adj. R²: 0.06891213837091581- Review: What is R-squared? What is adjusted R-squared?

R-squared

Adjusted R-squared accounts for the number of predictors in the model. It adjusts

- Question: Based on the adjusted

Answer:

- Main effects model Adj.

- Interaction model Adj.

The interaction model has a slightly higher adjusted

Thus, while the interaction model performs slightly better, according to Occam’s Razor, we may still prefer the main effects model unless the interaction effect is of specific interest or improves interpretability.

Another model to consider

- Your turn: Let’s add one more model to the variable – issue month. Should we add this variable to the interaction effects model from earlier?

model_with_month = smf.ols('interest_rate ~ credit_util * C(homeownership) + C(issue_month)', data=loans).fit()

print(model_with_month.summary()) OLS Regression Results

==============================================================================

Dep. Variable: interest_rate R-squared: 0.069

Model: OLS Adj. R-squared: 0.069

Method: Least Squares F-statistic: 106.5

Date: Mon, 05 May 2025 Prob (F-statistic): 5.62e-151

Time: 17:48:39 Log-Likelihood: -29919.

No. Observations: 9998 AIC: 5.985e+04

Df Residuals: 9990 BIC: 5.991e+04

Df Model: 7

Covariance Type: nonrobust

============================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------------------

Intercept 9.4870 0.211 44.861 0.000 9.072 9.902

C(homeownership)[T.Mortgage] 1.3921 0.228 6.115 0.000 0.946 1.838

C(homeownership)[T.Own] 0.7000 0.316 2.212 0.027 0.080 1.320

C(issue_month)[T.Jan-2018] -0.0799 0.121 -0.660 0.509 -0.317 0.157

C(issue_month)[T.Mar-2018] -0.0651 0.119 -0.546 0.585 -0.299 0.169

credit_util 6.2043 0.325 19.075 0.000 5.567 6.842

credit_util:C(homeownership)[T.Mortgage] -1.6384 0.457 -3.583 0.000 -2.535 -0.742

credit_util:C(homeownership)[T.Own] -1.0646 0.590 -1.805 0.071 -2.221 0.091

==============================================================================

Omnibus: 1157.710 Durbin-Watson: 1.984

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1631.442

Skew: 0.903 Prob(JB): 0.00

Kurtosis: 3.809 Cond. No. 20.8

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.Answer Based on the output of model_with_month, here’s how to interpret whether or not to keep issue_month in the model:

Adjusted R²: - Interaction model (no month): 0.0689

- With issue_month added: 0.0690

➡️ Change: +0.0001 — a negligible increase in adjusted R².

AIC Comparison: - Interaction model AIC: 59850.40

- Model with issue_month AIC: 59850.00

➡️ AIC improved by only 0.4 points, which is not meaningful.

Coefficient Significance for issue_month: - Only 2 months are shown (Jan-2018, Mar-2018), and both have high p-values (> 0.5), meaning they are not statistically significant predictors.

Conclusion (based on Occam’s Razor):

Although adding

issue_monthresults in a tiny improvement in AIC and adjusted R², the predictive value is negligible and the coefficients for months shown are not significant.

Therefore, we should not include issue_month in the final model.

The interaction model without it is simpler and performs just as well — and thus is the preferred model.